Komerční banka’s economic forecast – 2018: Richer Households, Stronger Koruna

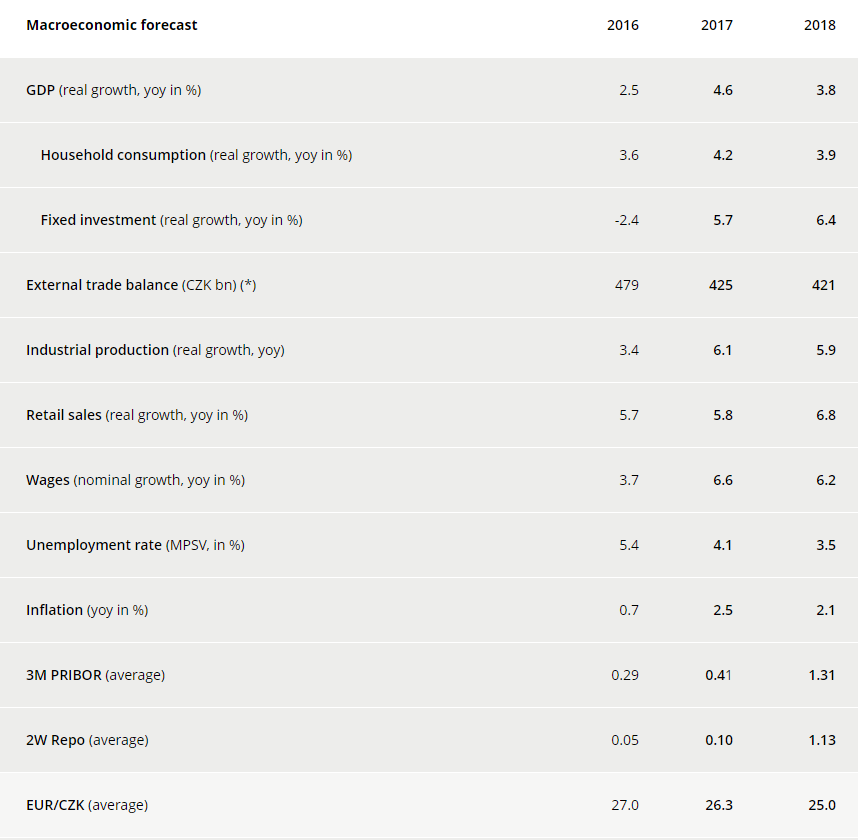

According to Komerční banka’s updated estimate, the Czech economy grew at a rate of 4.6% last year. “This means that the second best result for the past decade was achieved,” notes Jan Vejmělek, Komerční banka’s Chief Economist. A truly unique constellation, where all components of demand contributed to the growth, was behind this success. In particular the end of last year was a pleasant surprise and it lays good foundations for this year again. “We have therefore revised the outlook for this year for the better as we expect the economy to grow by 3.8%. Our estimate is one of the most optimistic in the market,” adds Jan Vejmělek.

Household consumption and the public sector’s strong investment activity will be the predominant factors of the Czech economy’s growth this year. According to Viktor Zeisel, a Komerční banka economist, tensions in the labour market will be the main mover of this year’s macroeconomic developments in the Czech Republic. The reason is that the lowest-ever rate of unemployment generates strong pressures for wage increases. Together with the appreciating koruna, these are the most important risks for domestic manufacturers’ price competitiveness.

“The only way to counter the shortage of labour and its increasing cost is investing in productivity. And Czech companies have understood this: their investment appetite was really strong last year.”

While over the past two years public investments lagged behind both our own expectations and the approved national budget, we believe that the situation will change.

“This year, the government must draw a part of the money from EU funds; otherwise, it will be deprived of the money. The government can also use the hundreds of billions in budgeted but unspent expenditure from preceding years if capital projects are actually launched at last. Both of these factors can be a strong driver for this year’s investment activity in the public sector. The requirement that investments must first be financed using the national resources, together with deploying the money held in unspent budgeted expenditure, can, however, cause the country’s budget to end up worse than approved for the first time since 2011.”

The central bankers can be satisfied with the development of inflation this year. While the average rate of inflation was 2.5% last year, we have revised the outlook for this year slightly downwards to 2.1% on average. Thus, the year will see inflation gradually returning to the 2% inflation target, in the direction from the above. In the light of strong internal demand, achieving the target will also be helped by the tightening monetary conditions. The CNB was the first central bank in Europe to start to hike rates in mid-2017. “This year we expect that the CNB will hike rates at each of its main meetings,” claims Viktor Zeisel adding that, however, the new forecast produced by the CNB will not indicate this. “I expect rate hikes from the CNB’s meeting on 1 February, but the overall tenor of the meeting will be dovish,” adds Viktor Zeisel.

A combination of a robust economic growth, tightening monetary policy and larger issuance of government bonds will result in rising bond yields.“The period when the government was borrowing at negative interest is clearly over. In our opinion, yields from the 10Y government bond will exceed 2% this year,” clarifies Marek Dřímal.

The continuing rapid economic growth and the continuously rising interest rates will be the main driver for Czech koruna’s strengthening. The CNB will resume its practice of publishing its forecasts of the FX rate development. “We expect the CNB to point to an appreciating currency in its forecast. For this year, we ourselves expect the koruna to appreciate to less than CZK 25/EUR, or CZK 20/USD,” says Jan Vejmělek.

The external environment is evolving favourably. Central banks in the US and the euro area will continue reverting to a normal functioning. According to Jana Steckerová, a Komerční banka economist, ECB will exit the QE programme this year. “This should enable the euro to keep its recent gains against the dollar and strengthen to USD 1.27/EUR this year,”predicts Jana Steckerová.

Note: (*) external trade as per cross-border statistics