Currency Option Strategies

Execute a series of currency forwards at better than standard exchange rates

Zero initial cost

A team of experienced professionals

at your service

at your service

Execute transactions over the telephone – in any currency offered by KB

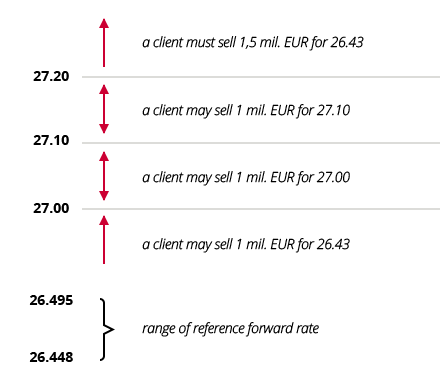

Benefit from better exchange rates with a correctly selected strategy

Monitor your transactions with confirmations

Risks warnings: The derivative instrument in question may be outside the client’s target market. This product is primarily aimed at hedging against market risk. Always pay close attention to the parameters of this product and its risks.

Risks warnings: The derivative instrument in question may be outside the client’s target market. This product is primarily aimed at hedging against market risk. Always pay close attention to the parameters of this product and its risks.

More information about risks